The cost of pacemakers and other cardiac devices

Considering getting a pacemaker in a private hospital? The last thing you should be worrying about is your cover. Give us a call and let us help you look for a policy today.

- Australian owned and operated call centre

- Speak to an expert right away

- A quick call could save weeks of research

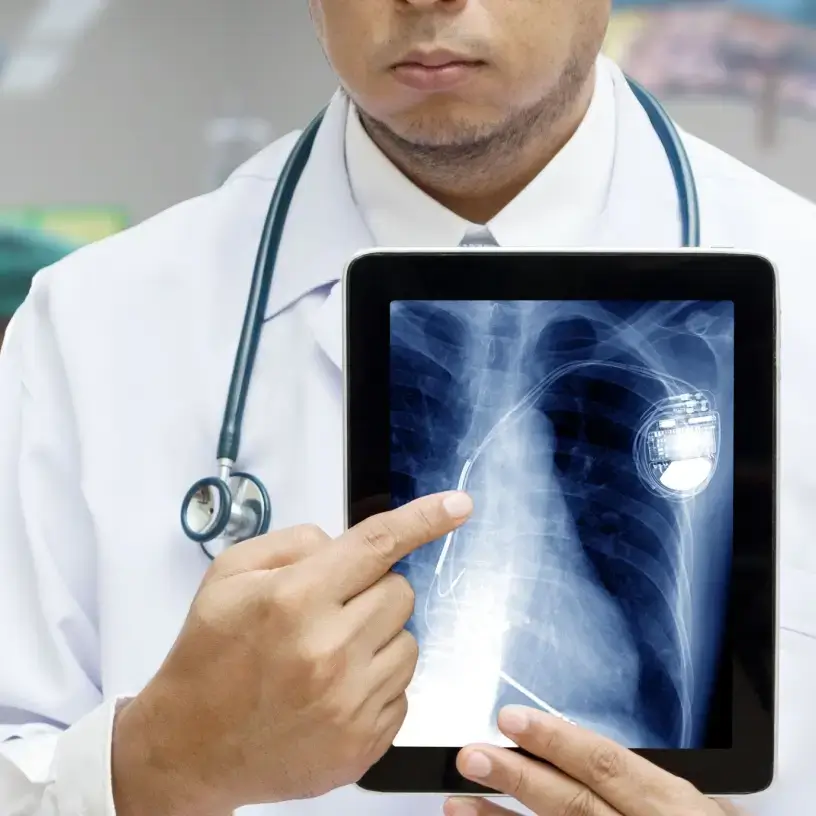

What is a pacemaker?

A cardiac pacemaker is an electronic device threaded through the veins to the heart, comprising of electrodes, a battery, a pulse generator and a small computer.2 These devices help improve heart function by sending electrical impulses to control your heart rate. A pacemaker can treat conditions such as:

- An irregular heart rhythm (arrhythmia)

- A slow heart rate (bradycardia)

- Some types of heart disease.

However, it’s not the only type of implantable cardiac device. Artificial implantable cardioverter defibrillators (AICD) monitor for dangerous irregular heart rhythms and send an electric shock to manage a heart that’s in fibrillation (i.e. beating irregularly).3 Another type of pacemaker called a cardiac resynchronization therapy device (CRT) or a biventricular pacemaker assists people with heart failure by stimulating both of the lower heart chambers.4

Expert tips on private health insurance for pacemakers and cardiac devices

Our health insurance expert, Steven Spicer, has some tips on how private health insurance could help with your pacemaker surgery.

Steven Spicer

Executive General Manager – Health, Life & Energy

Consider a lower excess if you’re planning a surgery soon

Is it likely you’ll need a pacemaker in the near future? While you might pay a bit more for the premiums now, it may be best to look at policies with a lower excess to pay when you go into hospital. It could save you money in the long run, and you can always increase it at a later date. Just keep in mind that when you lower your excess, you will be required to serve any relevant waiting periods before it applies.

Take out health insurance early to allow time to serve the waiting periods

If you need a pacemaker or similar device, the last thing you’ll want to worry about is whether your surgery is included on your policy, or if you’ve served all the relevant waiting periods. The waiting period could be up to 12 months to be treated for a pre-existing condition as a hospital inpatient, so it’s a good idea to plan ahead.

Look for a specialist that aligns with your health funds gap cover

If you’re planning to be admitted to hospital for pacemaker surgery, it’s a good idea to contact your health fund for a list of doctors and specialists who align with their gap cover agreements. In many instances, you’ll only incur a minimal gap, or potentially none at all, if the healthcare provider participates in your fund’s gap cover scheme.

Costs and cover

What is the cost of pacemaker surgery?

Most healthcare providers consider pacemaker implantation to be a relatively minor surgery, and it’s usually priced as such. For patients privately insured for this procedure who were treated in a private hospital, around 43% had no out-of-pocket doctors’ fees for their pacemaker surgery.5 The typical out-of-pocket cost for the other 57% was approximately $50. While this doesn’t include hospital fees (which average around $17,000), most or all of these fees can be covered by your health fund.

While the procedure cost is quite reasonable, there may be other costs that you need to consider, which will vary based on your circumstances and policy. For example:

- Excess. An excess is only paid when you claim on your private hospital insurance. You decide what amount this excess will be (or whether you’ll pay it at all) based on the options available when choosing your hospital insurance. For example, you might choose a $250 excess, which you will be required to pay if you make a claim. The higher your excess, the lower your premiums will usually be for the same policy, and vice versa.

- Co-payment. A co-payment is a charge you may have to pay every day of your stay in the hospital to your insurer, often up to a capped amount. For example, you may pay $50 each day you’re admitted as a private hospital patient.

- Miscellaneous costs. It’s important to consider the ancillary costs of undergoing such a procedure, such as out of pocket costs, parking, babysitting or loss of income if you need to take a few weeks off work.

Should I take out private hospital insurance for pacemaker procedures?

The average cost paid towards private patient pacemaker insertion surgery (which is typically paid by private health insurers, provided the patient has an appropriate level of cover) for accommodation, theatre and medical device fees is $17,000.5 Keep in mind that pacemaker costs for private patients may exceed what the fund pays and you may need to pay any gap and excess costs as well as incidentals.

Ultimately, it’s up to you whether you want to go public or private. However, the private system might be worth it if you’d like to choose your own doctor, recover in a private room (if available) and avoid the public system’s waiting lists. In short, with private health insurance, you can undertake the procedure on your terms.

If you’re trying to figure out which policies might suit your particular health needs, check our guide to the different private hospital insurance categories, which explains which tiers cover which services and can help you decide whether this purchase suits your needs.

Are pacemakers covered by Medicare?

If it’s medically necessary and you’re admitted to a public hospital as a public patient, Medicare will cover the total cost of your surgery. However, this will also mean:

- You must enter the public waiting list for this procedure, which is typically longer than the private system.

- You cannot choose your doctors (e.g. cardiologist, anaesthetist).

- You would be unlikely to have a private room during your hospital stay.

Compare Health Insurance Now

Compare health insurance options through our simple-to-use service and look for a policy that suits your needs.

How pacemaker surgery works

How pacemaker surgery is done

Like many cardiology procedures, people are often concerned about complications and ask if pacemaker surgery is dangerous. While all surgeries carry some degree of risk, you might be surprised to hear that pacemaker surgery is a relatively safe and non-invasive procedure.

Like many cardiology procedures, people are often concerned about complications and ask if pacemaker surgery is dangerous. While all surgeries carry some degree of risk, you might be surprised to hear that pacemaker surgery is a relatively safe and non-invasive procedure.

To implant a pacemaker, a doctor will make a small incision around the collarbone to access a major vein close to the heart. They will then use an x-ray to guide the electrodes to the heart, where they will attach them to the pacemaker and heart.

The surgery typically takes one to three hours. You may be required to stay in the hospital for a day after the procedure so the doctors can monitor your heart and make any necessary adjustments to your pacemaker.3

Who would need a pacemaker?

While it’s ultimately a decision between you and your doctor, there are a few circumstances where you might want to consider a pacemaker. If you have an irregular or weak heartbeat, or you suffer from a heart disease, your doctor may recommend a pacemaker.

You’ll also want to discuss with your doctor to whether you’ll get a temporary or permanent pacemaker. This will depend on the type and severity of your condition.

Meet our health insurance expert, Steven Spicer

As the Executive General Manager of Health, Life and Energy, Steven Spicer is a strong believer in the benefits of private cover and knows just how valuable the peace of mind that comes with cover can be. He is passionate about demystifying the health insurance industry and advocates for the benefits of comparison when it comes to saving money on your premiums.

Want to know more about health insurance?

1 Australian Institute of Health and Welfare – Heart, stroke and vascular disease—Australian facts. Last updated June 2023. Accessed May 2024.

2 Healthdirect, Pacemaker. Last updated October 2022. Accessed May 2024.

3 Mayo Clinic – Implantable cardioverter defibrillators. Last updated August 2023. Accessed May 2024.

4 Mayo Clinic – Cardiac resynchronization therapy. Last updated July 2023. May 2024.

5 Department of Health, Medical Costs Finder. May 2024.

Talk to an expert

At a time that suits you

Call now