We'll arm you with the tools you need to make the right choice for you. From property reports to credit scores, let's work together to make your property dreams come true.

Dreaming of owning a property? Let's find out how much you can potentially borrow to put towards your new purchase.

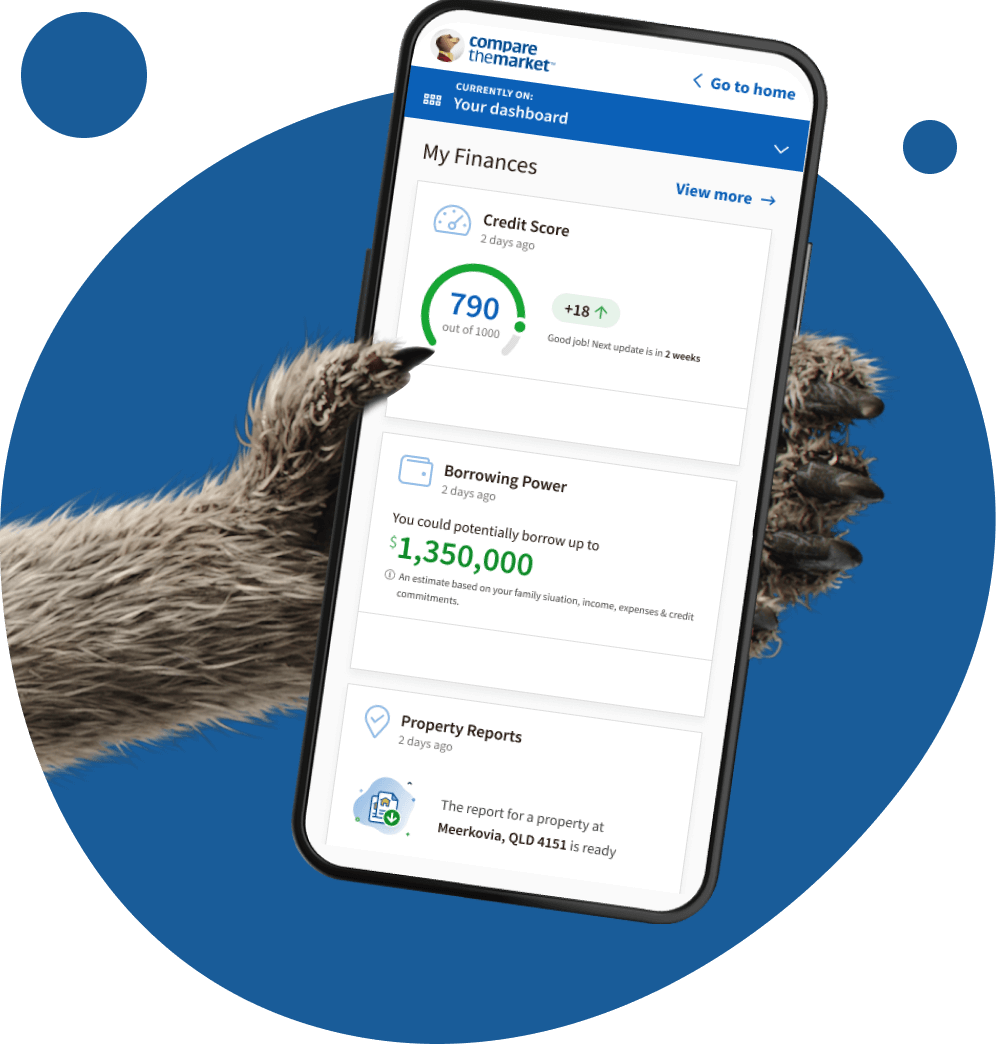

Get the same credit information that lenders, telcos and utility providers use to assess your creditworthiness without impacting your actual score.

Buying, selling or being a nosey neighbour? Get valuable insights about the property, view recent sales and more.

Ready to buy or refinance? Apply online via a single application and we'll instantly check your eligibility for a home loan from a wide variety of lenders on our lender panel.

Our Meerkat Technology makes our comparison and application process a breeze, but sometimes you just need a helping hand! Our team of brokers and home loan experts are here to bring ease and expertise, and no question is too big or small; we're happy to help!

From the meerkats who made insurance and energy Simples comes a new way to compare and apply for a home loan. Welcome to Home Loan Heaven.

Say farewell to endless paperwork. In Home Loan Heaven you can compare from a range of lenders and then apply for a home loan completely online.

Our powerful lender-matching engine assesses your eligibility against the lender’s criteria. Instead of a laundry list of loans, you’ll see only those you’re eligible to apply for.

Keep your credit scores, property and suburb reports, loan comparisons and borrower scenarios all saved and easily accessible in your Home Loans Dashboard.

Our experts are on hand if you need help with your application, plus they also work hard behind the scenes with our panel of lenders to help you get a better deal and make the application process run smoothly.

Meet our brokers“My wife and I use Compare the Market for all our household expenses, and we’re in good company - over the years, they’ve helped millions of Australians find a better deal.”

It’s simple; there are thousands of home loan options in the market making it harder to figure out which loan is right for you. Rather than going with the first loan you find, you can go with a loan that suits your circumstances.

Whether you’re a first home buyer looking for a new home, an investor, or you’ve bought before and are looking to refinance, our free service can help you take the next step with confidence.

Finding a competitive interest rate has never been so simples!

Selling Houses Australia host, Andrew Winter explains how home loans work, and covers off some basics that prospective homebuyers need to know.

To get the most out of our comparison service, all you need to do is provide some basic details about your specific circumstances. Then we’ll show you a range of home loans products we think might be suitable for you based on the information you’ve given to us.

Whether you’re buying your first home, a new home, or looking to refinance, we’ve got a really simples way to help you find a home loan that suits your unique needs and circumstances!

Compare home loans Thinking about switching home loans but unsure if you’re ready to take the plunge or not? We can help you figure out if it’s the right move for you, as well as answer some common questions you may have regarding refinancing.

Learn moreTo fix, or not to fix? That is the question, and it’s just one of many we may be able to help you with! Learn more about fixed rate home loans and their various pros and cons here.

Learn moreWhoever first said a change is as good as a holiday must’ve had a variable rate home loan! If you're weighing up your home loan options and considering a variable rate product, understand the key details with the help of our variable rate home loan FAQs.

Learn moreYour LVR can have a big impact on the ultimate cost of your home loan – but what is it in the first place, and how do you figure out what yours would be? Our LVR FAQs can help you figure out the answers.

Learn moreIf you’re hoping to land a foot on the property ladder and buy your first home, you’ll want to make sure you’re putting your best foot forward. You can arm yourself with all the information you need with the help of our dedicated info hub for first home buyers.

Learn moreStamp duty can tack a significant amount onto your home loan – but how do you figure out how much you might have to pay, or whether you’ll have to pay it at all in the first place? We’ve got the answers.

Learn moreA home loan is money you borrow from a lender to buy a property if you don’t have enough funds to cover the full purchase price. You then repay this borrowed amount over the length of your loan (generally over 25 to 30 years), in regular instalments that includes interest.

Interest on the loan is charged at either a variable rate (which can fluctuate with the market) or a fixed rate (usually set for 1 to 5 years) or a combination of the two. Because interest is added, the total amount you pay back to the lender will likely be significantly larger than the size of your home loan.

A comparison rate calculates the interest rate with fees and charges on a home loan to show the ‘true cost’ of the loan. Because it includes any extra costs, it can differ from the advertised rate by a substantial amount and gives a more accurate figure than the interest rate alone. This makes it easier for borrowers to compare different loans and lenders.

Financial institutions are legally required to display a comparison rate next to any advertised home loan interest rate to allow for easy comparison for consumers. They must also display a comparison rate warning whenever they’re offering home loans to show customers how the comparison rate is calculated. The formula used to calculate comparison rates is standardised across all lenders and products.

A home loan is simply the amount of money you’ve borrowed to purchase your home, whereas a mortgage is the legal agreement that you have to sign before receiving your home loan. The mortgage essentially gives the lender a security interest over the property, meaning while you legally own the property, the lender has the right to repossess and sell the property if you fail to make your repayments.

This means, for example, that if you failed to maintain your home loan repayments and ended up defaulting, the lender has the legal right to repossess the property and sell it.

Even though a mortgage and a home loan technically describe different aspects of this legal encumbrance and associated financial product, you can’t really have one without the other, so it’s common to use the two terms interchangeably.

The common types of home loans are principal and interest loans, interest-only loans, owner-occupier loans, investment loans, bridging loans and construction loans. They differ based on how you repay them, how interest is charged, and whether the property is owner-occupied or used for investment.

Some options may suit you better than others, depending on your financial priorities and needs. The most common types of home loans include:

Note that some of the above loan types aren’t mutually exclusive. For example, you could have an IO investment home loan, or a P&I owner-occupier home loan – there’s a difference between a loan’s purpose and the type of payments it requires.

You can speak to one of our home loan specialists if you’d like to learn more about what kind of home loan might be suitable for you.

There are two main types of home loan interest rates: fixed rate and variable rate home loans, and then there are also split-rate home loans, which combine the two. Each type has its advantages and trade-offs. Your choice can affect how predictable your repayments are, and how your loan responds to Reserve Bank of Australia (RBA) rate changes.

When you’re comparing loans, always check the comparison rate. It combines the advertised rate with the loan’s fees and charges, to give you a clearer sense of the true overall cost.

Home loan calculators are digital tools that help you estimate your borrowing power, home loan repayments, upfront costs such as stamp duty and lenders mortgage insurance, as well as access property reports.

We offer a range of home loan calculators to help you plan and compare your options if you’re looking to crunch some numbers before you start looking for a home loan.

Our range of home loan calculators and tools is user-friendly and suited to borrowers of all kinds, from first home buyers to refinancers and property investors.

We’ve got calculators to help you at every stage of the homebuying process:

We also have a stamp duty calculator for every state and territory in Australia:

A good home loan generally combines competitive interest rates with useful features, such as an offset account or redraw facility, to help reduce the amount of interest you pay or give you flexibility if your financial situation changes – whether you’re an owner-occupier or investor.

While the interest rate (comparison rate) is undoubtedly an important factor, other features such as repayment flexibility and extra repayment options can make a big difference over time by helping keep your overall costs down and giving you greater control over how you manage and repay your loan.

Depending on your needs and circumstances, some common features to look for include:

If you’re unsure as to which features you might need on a home loan, you may want to speak to an expert or do your own research before beginning your home loan journey.

To apply for a home loan, you’ll usually need to work out your borrowing power, compare rates, and gather your financial documents to submit an application. You can start the process by going directly to a lender or using our home loan comparison tool and speaking to one of our home loan specialists, who can then guide you every step of the way, from getting a home loan pre-approval through to settlement.

Whether it’s your first home loan or your 15th, the application process is usually pretty similar and may involve:

A mortgage broker is a financial professional who helps you find and apply for a home loan. They act as a kind of ‘project manager’ for your home buying (or refinancing) process, overseeing the loan application from pre-approval to settlement while handling all the necessary liaising with the lender on your behalf, including providing information on additional payments you might be eligible for, such as the First Home Owner Grant or stamp duty concession.

Even if you feel you’ve got a fairly firm grip on the whole homebuying process, enlisting the services of a mortgage broker could be prudent for a few reasons. Many brokers have built up strong relationships with certain lenders, meaning they’re well-placed to negotiate on your behalf and potentially secure you a better deal.

Luckily for you, our experienced brokers are ready to help you with your home loan application whenever you’re ready. During your journey within our home loan comparison tool, you can ask to be put in touch with one of our mortgage brokers, and they’ll be able to answer any questions you have about the products or process in front of you.

Home loan pre-approval involves your lender making a non-binding indication that they would lend you the money needed to buy a house once you find it, based on an initial review of your income, expenses, debts, assets, and credit history. It helps you understand your borrowing power before you go house hunting, but it’s not final approval or a guarantee that your loan will go ahead.

Borrowers typically seek pre-approval to align their home search to a clearer budget and to be better prepared for auctions or making offers. Pre-approval is generally free and often valid for 60 to 90 days.

You can apply for home loan pre-approval from as many lenders as you’d like but each separate application could put a small dent in your credit score, so it’s usually best to limit the number of applications.

First home buyer grants and concessions are government incentives that reduce upfront property-buying costs and lower deposit requirements by giving you extra cash or cutting down on expenses such as stamp duty.

Depending on where you plan to buy and whether you’re building or buying a new or existing property, you may be eligible for a combination of incentives that can significantly reduce how much you need to pay upfront. Because eligibility rules, property price caps and support amounts vary by state and territory, it’s important to check what’s available in your area before applying for a home loan.

Some of the key government support options available to first home buyers include:

1. First Home Owner Grants (FHOG), a lump sum paid by your state or territory government towards the cost of your first home (given you meet the relevant eligibility criteria).

While the exact conditions and amounts will vary depending on where you live, you can typically be confident that you may receive a grant of at least $10,000 if you meet the relevant eligibility requirements.

The notable exception to the grant is the ACT, which scrapped its FHOG for property transactions entered after 1 July 2019 and now offers significant stamp duty concessions to its first home buyers instead. This means instead of being given extra money to put towards your purchase, you’ll pay less money when it comes to that pesky property transfer tax.

2. Stamp duty discounts. You’ll generally have to pay stamp duty when buying a house, which can add up to thousands or even tens of thousands of dollars. Stamp duty, also known as transfer duty, is essentially a tax on the sale and transfer of property and land.

Most states and territories offer significant stamp duty concessions and discounts for first home buyers.

3. The Australian Government 5% Deposit Scheme: Formerly known as the First Home Guarantee, the Australian Government 5% Deposit Scheme lets eligible Australians buy their first home with a deposit of 5%, and single parents or legal guardians with a deposit of just 2%. The federal government then guarantees the lender up to 15% of the property value (or up to18% in case of eligible single parents or legal guardians), which means you (the borrower) may not have to pay for lenders mortgage insurance.

Home loans generally come with a range of upfront and ongoing fees to cover the costs of processing and managing your mortgage, such as an establishment fee, a valuation fee, and lender mortgage insurance (LMI) if your deposit is less than 20% of the property’s value.

While some home loans are marketed as ‘low-fee’ or ‘fee-free’, there’s unfortunately no such thing as a truly fee-free home loan. Even if you avoid paying ongoing monthly fees on a ‘fee-free’ home loan, you’ll typically still have to cover a handful of upfront fees.

Some common home loan fees to be aware of include:

Make sure you read the key facts sheet for more information on the fees and charges for any given loan, and check the comparison rate to understand the true cost of your loan. While you typically can’t avoid paying home loan fees outright, you can shop around to find a loan with competitive fees that beat the competition and suit your financial priorities.

Lenders mortgage insurance (LMI) is a one-time fee your lender may charge if your saved deposit is below 20% of the property value (meaning your loan-to-value ratio is higher than 80%). While you pay the cost, LMI acts as insurance for your lender, providing a financial buffer if you can’t meet your home loan repayments.

In many cases, the cost of LMI is added to your loan amount rather than paid upfront. While this helps in preserving cash for other upfront costs, it increases your loan balance, meaning you’ll end up paying more interest over the life of your loan. Capitalising LMI can also push you into a higher LVR bracket, triggering an even higher base LMI fee in the first place.

It’s worth noting, however, that you may also be offered the option of paying your LMI upfront, which could reduce the overall cost of borrowing.

Your loan-to-value ratio (LVR) is the amount you’re either wanting to borrow or have already borrowed, expressed as a percentage of your property’s value.

For example, if you were to borrow $400,000 in order to purchase a $500,000 property, you would have borrowed 80% of the property value, giving you an LVR of 80%.

It’s important to consider the LVR before you get the ball rolling on any home loan applications, as it can have a significant effect on the outcome of your efforts to get a home loan.

An unfavourable LVR may see you charged a higher interest rate, or even sink your application entirely and result in a denial by the lender.

Refinancing is the process of replacing your current home loan with a new, better-value home loan, either with your existing lender or a different one. People often refinance to get a lower rate, better features, more flexible repayments, tap into home equity or roll higher-interest debts into one loan.

A home loan that felt like a great deal a few years ago may not suit your needs today as interest rates, loan products, and your financial circumstances change over time.

Refinancing gives you the chance to reassess your current loan and switch to one that better fits your financial situation. If you decide to refinance, funds from your new loan will generally pay off your existing loan. The old mortgage is then discharged, and a new mortgage is registered over the same property.

As always, you should be sure to compare a range of options before committing to one – you can begin your search using our home loan comparison tool.

Before buying an investment property, it’s important to understand your financial situation, the property’s rental income potential, and its long-term returns.

Investment loans generally come with higher interest rates and stricter lending criteria than owner-occupier loans. That’s why it’s worth looking closely at both rental yield and capital growth potential, as they can help you estimate how profitable a property might be by comparing the income you expect with the costs of owning and maintaining it.

In some cases, the interest charged on an investment property loan may be tax-deductible, which is why an interest-only loan can form part of certain investment strategies. However, tax rules can be complex, and you’ll typically want to consult with an accountant or financial adviser before trying any tricky taxation tactics.

If you’re looking to buy an investment property rather than a home, our property investing guide contains a wealth of valuable information, including:

Interest on investment loans may be tax-deductible, which can form part of a broader investment strategy. However, it’s important to seek advice from a qualified accountant or financial adviser.

There’s no one ‘best’ home loan in Australia, as the mortgage for you is the mortgage that meets your financial priorities and needs. This generally means it has a competitive interest rate and fees and comes with high-value features you’ll use, that don’t cost an arm and a leg.

All that being said, it can be difficult to know what a high-value loan looks like if you’re a first-home buyer or haven’t had to shop around for home loans in a while. But have no fear – our free to use, no-obligation home loan comparison service can help you on your search for the right home loan, from start to finish.

If you’re looking to buy a house, you might be interested in knowing which areas are the most affordable – and conversely, which suburbs are astronomically expensive.

As per Cotality’s most recent annual Best of the Best report, these were the cheapest and most expensive suburbs for buying a house in each Australian state and territory (by median value) in 2025. Cotality’s research is based on property data provided by state and territory governments. The figures below represent median house value for each suburb listed.

Source: Best of the Best 2025: Top Aussie Suburbs Revealed – Cotality

Stephen has more than 30 years of experience in the financial services industry and holds a Certificate IV in Finance and Mortgage Broking. He’s also a member of both the Australian and New Zealand Institute of Insurance and Finance (ANZIIF) and the Mortgage and Finance Association of Australia (MFAA).

Stephen leads our team of Mortgage Brokers, and reviews and contributes to Compare the Market’s banking-related content to ensure it’s as helpful and empowering as possible for our readers.

Let's get started making your property dreams a reality!

Click the button below to begin your home loan journey.