It’s never been quicker or easier to do a financial health check

Have you checked your credit score recently? If not, here’s the push you needed, because we’re here to help.

Our credit score tool is secured using Verification of Identity (VOI) technology, meaning the only person finding out about your credit score will be you.

You’ll be able to track how your credit score has changed over time and identify any anomalies or trends.

We’ll let you know every month when your new and updated credit score is ready to view, to help you stay across your financial health.

Our credit score tool is completely free to use – you could check your credit score with us a million different times and it wouldn’t cost you a cent.

Our Meerkat Technology makes our comparison and application process a breeze, but sometimes you just need a helping hand! Our team of brokers and home loan experts are here to bring ease and expertise, and no question is too big or small; we're happy to help!

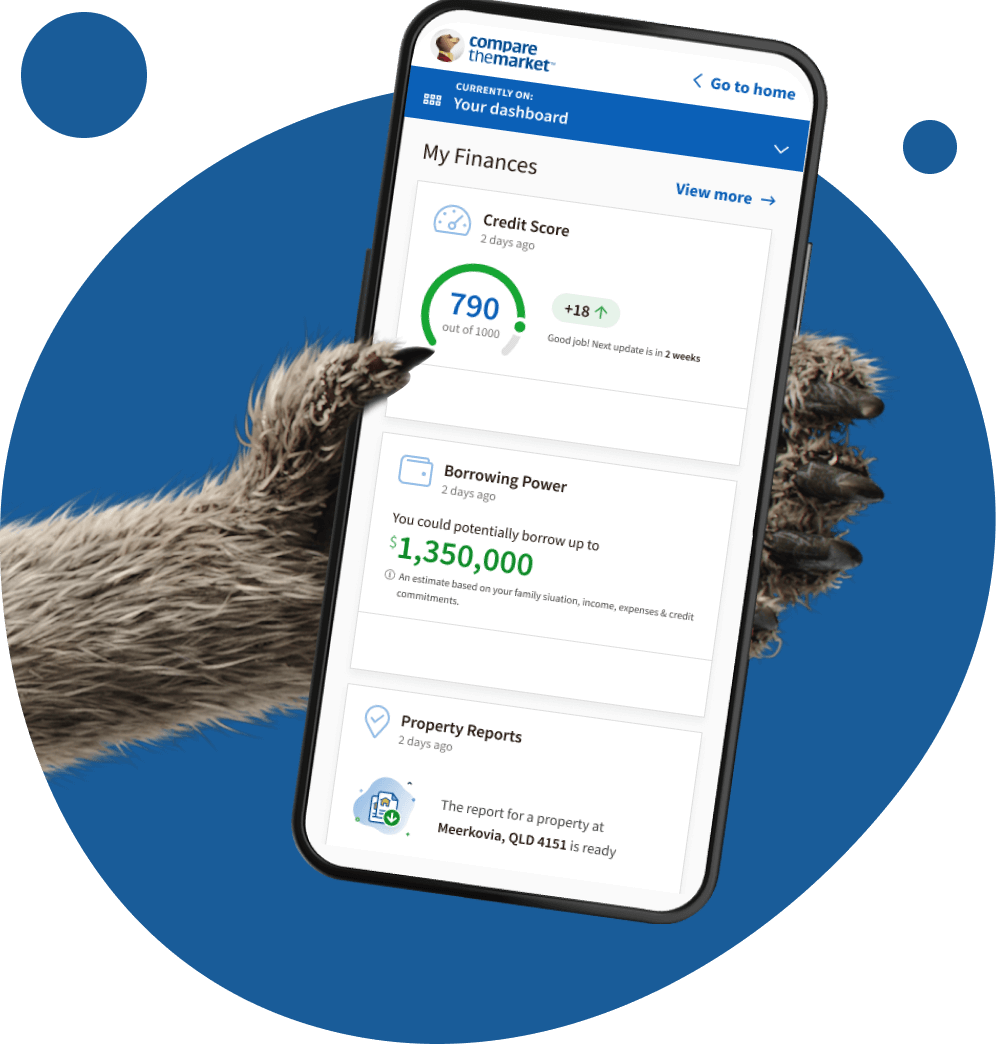

We'll arm you with the tools you need to make the right choice for you. From property reports to credit scores, let's work together to make your property dreams come true.

Dreaming of owning a property? Let's find out how much you can potentially borrow to put towards your new purchase.

Get the same credit information that lenders, telcos and utility providers use to assess your creditworthiness without impacting your actual score.

Buying, selling or being a nosey neighbour? Get valuable insights about the property, view recent sales and more.

Ready to buy or refinance? Apply online via a single application and we'll instantly check your eligibility for a home loan from a wide variety of lenders on our lender panel.

Credit scores can be a complex subject, but property expert and host of Selling Houses Australia, Andrew Winter, is here to help simplify them for you.

Andrew Winter shows you how to use Compare the Market’s free credit score tool, and walks you through its features and benefits.

Knowledge is power! Whether you’re viewing your credit score for the first time or you’d just like to check in on it, we’ll retrieve it for you in minutes along with tailored insights into your credit report.

Get your free Credit Score & Report Your credit score is a number assigned to you based on financial information regarding your credit history, which is contained within your credit report. Depending on which credit reporting agency you’ve asked to calculate your score, the number will be between either 0 and 1,000 or 0 and 1,200 (the higher the better).

There are three main credit reporting agencies operating in Australia: Equifax, Experian and Illion. Each agency uses a different set of calculations when figuring out someone’s credit score, but each one will take the information contained in your credit file and plug it into their algorithm to end up with a final score.

These algorithms will generally weigh the merits of your financial history and habits (e.g. responsible credit management, making your repayments on time) against the cons of your financial history (like late repayments, credit defaults and credit applications) to determine your credit score.

Your credit score functions as a holistic overall representation of your creditworthiness. Lenders can look at where your credit score sits and immediately gain an idea of the amount of risk they’d be taking on by approving you for a loan or credit product.

Your credit score will be one of the primary factors taken into account by a lender if you apply for a home loan or credit with them. While every lender’s lending criteria will vary, you can bet your bottom dollar they’ll all look at your credit score and weight it heavily during their risk calculations.

Your credit score may even come into play in non-financial situations, such as applying for a lease on a rental property or setting up a new electricity or gas account with a utility provider. So, it pays to be across your credit score and working on improving it, even if it’s only in little ways.

A number of different factors will affect your credit score, so we’ve broken them down into things that will positively affect your credit score and things that will negatively affect your credit score.

| Good for your credit score | Bad for your credit score |

|

|

Improving your credit score, which is sometimes known as credit repair, is generally a long-term process. That being said, it’s also generally a pretty straight-forward process.

While there’s no instant way to raise your credit score, there are some things you can do that may see your credit score go up in the medium- to long-term:

Improving your credit score basically boils down to acting responsibly with your finances, not spending more than you earn and being able to demonstrate reliability and trustworthiness when it comes to debt and credit.

An unfavourable credit score generally won’t affect your quality of life on a day-to-day basis; however, it will almost certainly affect your chances of being approved for a line of credit or loan until you take active steps to improve your score.

So, if you’re hoping to take out a credit card or a home loan in the future and you have what could be considered a bad credit score, you may want to work on improving it before making any applications.

A higher credit score could improve your likelihood of being approved for a home loan or line of credit, and potentially for rental applications as well. It can also influence the amount of credit you can expect to be approved for; for example, your credit limit or loan interest rate may be influenced by your credit score.

It’s worth noting that while your credit score can have a huge impact on your ability to do certain things, a lower credit score is by no means a death sentence or a personal flaw; you may simply not be able to take out a credit card or borrow money from a bank for the time being.

You can check your credit score right here using our new home loan comparison tool, which has a free built-in credit score checker and can retrieve both your credit score and an snapshot or your history in minutes. It can also give you tips on how to improve your score.

You can also run a credit score check by contacting your credit reporting agency of choice (via their website, email or phone) and requesting your credit score and/or a copy of your comprehensive credit report.

Different credit reporting agencies may impose varying costs or fees for providing you with your credit score, but Australians are entitled to a free credit score check every three months.⁴

Several online credit score providers exist where people can access their credit report and find out their credit score for free. These service providers will generally draw on credit reporting information from the three main agencies in order to calculate your credit score, but (potentially) without charging the same fees.

You can visit the CreditSmart website for a list of credit score providers that offer credit reports and credit ratings for free.

Each of the three credit reporting agencies operating in Australia has its own proprietary algorithms and credit score ranges, so what makes for a ‘good’ credit score will vary depending on which agency is calculating your credit score for you.

For instance, an Equifax credit score of 500 will be different to an Experian credit score of 500 as detailed below.

Equifax uses a scoring range that extends from 0 to 1,200:¹

Experian scores using a range that extends from 0 to 1,000:²

Illion uses a scoring range that extends from 0 to 1,000:³

A score of zero with Illion generally indicates a payment default or bankruptcy filing on your credit report.

The credit score tool within our new home loan comparison service is completely free to use, whenever you like. And while you’re there, you can also calculate your borrowing power, research properties of interest and more, all in the one place!

Our tool updates your credit score monthly, and lets you check it whenever you’d like, as many times as you’d like – but Australians are also entitled to a free credit report and credit check every three months.

As we mentioned previously, you can visit the CreditSmart website for a list of the credit score providers you can get free credit reports and scores from.

If you discover a mistake or inaccuracy on your credit report (such as a ‘missed payment’ on a bill you never received or a loan repayment default that never happened), you should contact the credit reporting agency or credit score provider you received the report from as soon as possible.

They will be able to assess the item and determine whether it should be there or not; if not, they will have it removed. They may decide it isn’t a mistake, in which case you can either accept their decision or contact the Australian Financial Complaints Authority to seek a resolution to the disagreement.

You can also have incorrect personal details corrected via the same process, such as your age or date of birth.

Your credit report is a list of your relevant credit information, financial behaviour and activities over the last few years (up to seven). Your credit score is the number a credit reporting agency assigns you based on their assessment of all the information in your credit report.

If you check your credit score via our home loan comparison tool or make an enquiry about your credit score with one of Australia’s credit reporting bodies, you’ll typically be able to ask to see both your credit score and credit report. While your credit score may be the more useful of the two, it’s worth taking a look at your credit report now and then to check there aren’t any mistakes or inaccuracies, which could be doing significant damage to your credit score unbeknownst to you.

Stephen has more than 30 years of experience in the financial services industry and holds a Certificate IV in Finance and Mortgage Broking. He’s also a member of both the Australian and New Zealand Institute of Insurance and Finance (ANZIIF) and the Mortgage and Finance Association of Australia (MFAA).

Stephen leads our team of Home Loan Specialists, and reviews and contributes to Compare the Market’s banking-relating content to ensure it’s as helpful and empowering as possible for our readers.

As General Manager of Money at Compare the Market, Stephen Zeller wants to help ensure that consumers understand their credit score and how to positively influence it. With that in mind, he has some tips for you to help you give your credit score a shine:

Knowing your credit score is a crucial part of putting together a rock-solid home loan application – click the button below to check yours today!

Get your free Credit Score & Report