Specialist doctors

Thinking about going private? Read our guide on specialist doctors or talk to one of our experts to help you get covered today.

- Australian owned and operated call centre

- Speak to an expert right away

- A quick call could save weeks of research

What is a specialist doctor?

In the healthcare industry, the term ‘specialist’ refers to a specific type of medical doctor who has completed specialist training and is registered as a specialist through the Australian Health Practitioners Regulation Agency (AHPRA).1

When you see a specialist with a referral from your GP, the specialist will usually send their recommendations or diagnosis to your GP, who will remain your primary physician. This allows your GP to coordinate your healthcare with other specialists or medical professionals and avoid prescribing you incompatible medications or treatments.

There is a large range of approved specialties that doctors can be trained and registered for, so it can be hard to know exactly what each specialist does. Here is a list of common specialisations and what they do:2

| Specialist | What they do |

|---|---|

| Radiologist | Uses medical imaging such as x-rays to diagnose and treat illness or injury. |

| Ophthalmologist | Diagnoses and treats eye damage and disease with surgery, glasses and contact lenses. |

| Cardiologist | Diagnoses and treats diseases or conditions of the heart and cardiovascular system, such as heart disease and heart failure. |

| Gastroenterologist | Diagnoses and treats diseases or conditions of the digestive system and diagnoses with endoscopies and other methods. |

| Oncologist | Diagnoses and treats cancer. Oncologists often focus on a specific area of cancer treatment (e.g. surgical, radiation or medical). |

| Neurologist | Diagnoses and treats nervous system disorders. The nervous system can include the brain, spine, nerves and muscles. |

| Orthopaedic surgeon | Diagnoses, treats and rehabilitates musculoskeletal injuries such as scoliosis, sports injuries and congenital disorders. |

| Psychiatrist | Diagnoses and treats mental health disorders through psychotherapy and medication. |

| Obstetrician/Gynaecologist | Often known as an OB-GYN, these doctors specialise in both obstetrics and gynaecology. They diagnose and treat medical conditions relating to pregnancy/infertility and the female reproductive system. |

| Urologist | Diagnoses and treats conditions relating to the urinary tract and male reproductive system. |

Private health insurance and specialists

Does private health insurance cover specialist appointments?

Your private health insurance may pay a benefit towards the cost of a specialist doctor if you’re admitted as an inpatient, hold an appropriate level of private hospital cover, and if the treatment is listed on the Medicare Benefits Schedule (MBS). The MBS is a list of item numbers assigned to medical services, with each item having an assigned cost that the government deems reasonable.

When you’re treated as a public inpatient in a public hospital, the entire cost of your treatment will be covered by Medicare, including your specialist fees.

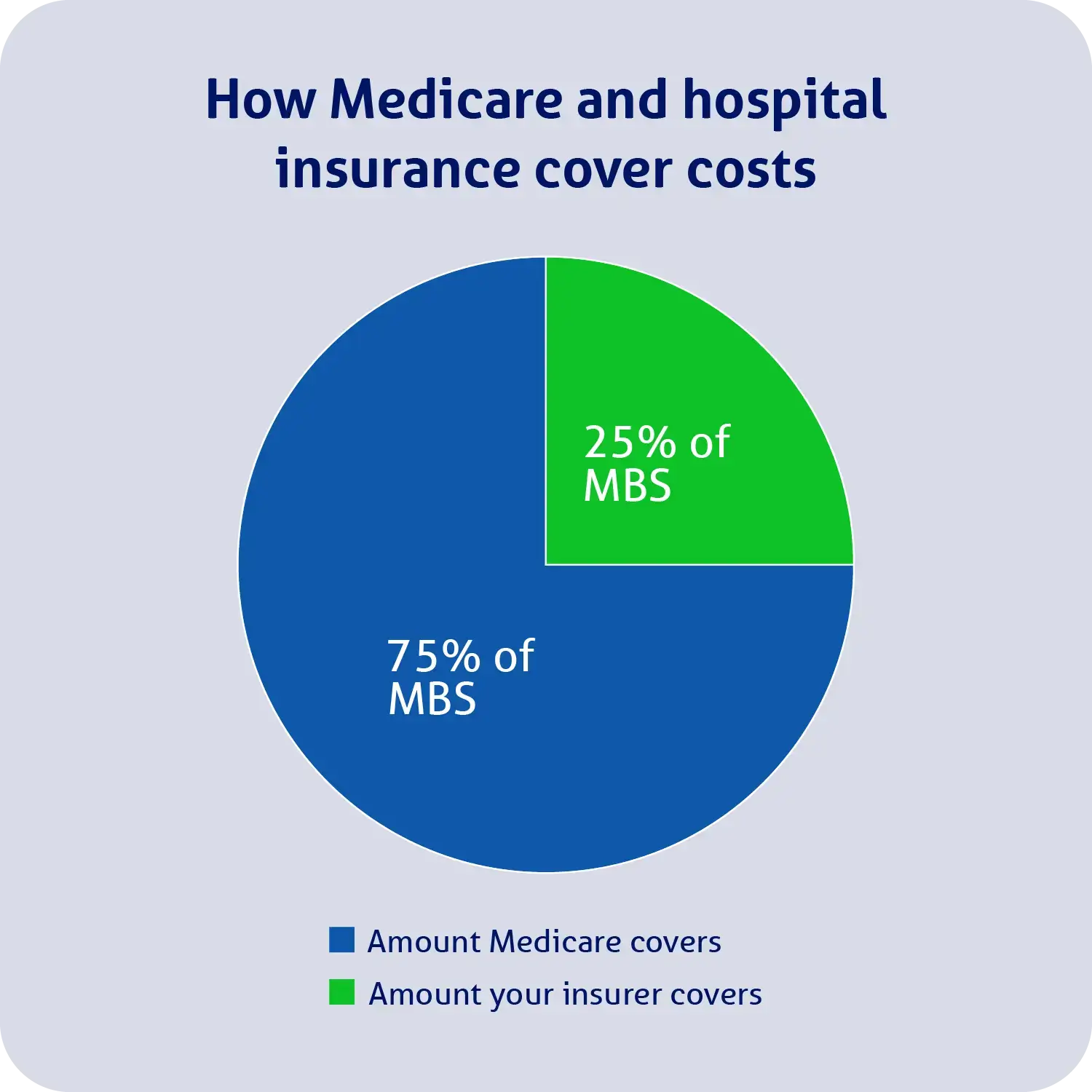

When you’re treated as a private inpatient in a public or private hospital, Medicare pays 75% of the MBS fee for your treatment. The remaining 25% could be covered by your private health insurance, provided you have a sufficient level of hospital cover and have served the relevant waiting periods.

For specialist treatments and consultations as an outpatient (i.e. not admitted to hospital) that are listed on the MBS, Medicare will typically rebate 85% of the MBS fee. By law, private health funds are not allowed to pay towards out-of-hospital medical services that are listed on the MBS and therefore covered by Medicare. However, there are some out-of-hospital services that Medicare doesn’t pay a rebate towards that can be included under an extras policy, such as physiotherapy and dental.

How does private health insurance cover specialists as an inpatient?

Private health insurance can pay a benefit towards costs when you’re admitted to hospital as a private inpatient, and your treatment is listed on the MBS. Medicare will rebate 75% of the treatment’s MBS fee, and your insurer can cover the remaining 25%.

See our example below:

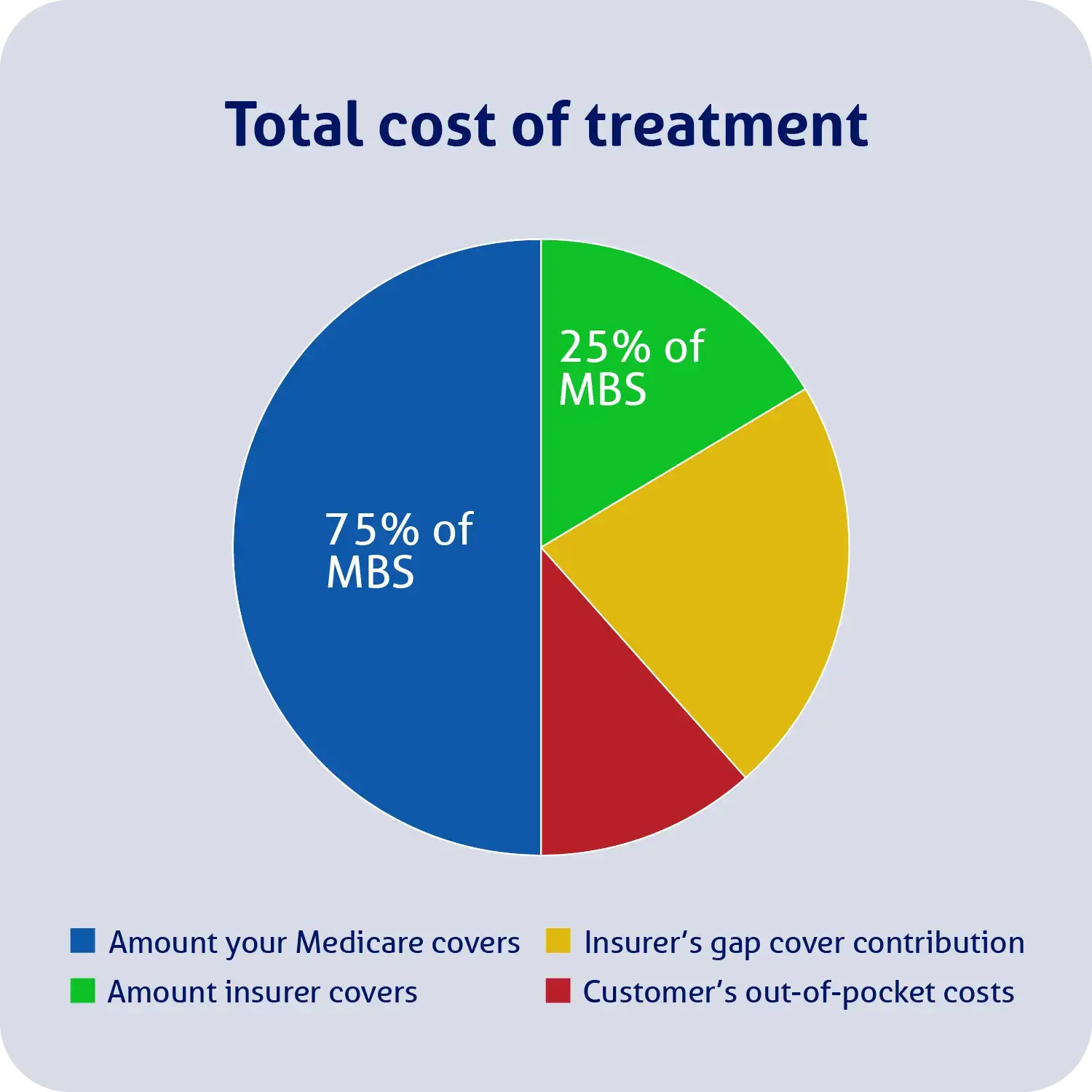

Keep in mind that specialists can charge you more for your treatment than what’s listed on the MBS (e.g. they could charge you $500 for your treatment, even though the MBS fee is $400).

As such, it’s possible that you may have some out-of-pocket costs, which are referred to as the gap.

You may be able to reduce or eliminate the gap if you participate in your insurer’s gap cover scheme. Most health funds have agreements with a selection of hospitals and doctors to reduce the out-of-pocket costs of their fund members. There are typically two types of gap cover schemes your doctor could participate in:

- No gap. Your health fund has a threshold above the MBS fee they are willing to pay if the doctor charges above the MBS but under the no-gap threshold. If your doctor agrees to this gap cover scheme, you should have no out-of-pocket costs for their services.

- Known gap. Limits your out-of-pocket costs so it won’t go over a set amount. Your health fund can inform you of this limit before you go in for treatment.

Keep in mind that it’s up to your doctor if they want to participate in your health fund’s gap cover scheme on a case-by-case basis. Therefore, it’s important to confirm this with your doctor before seeking treatment. It’s also a good idea to speak to your health fund prior to a hospital admission.

Below, we’ve included a visual example of how Medicare and your health fund may help cover the cost of treatment when the treatment cost is greater than its MBS fee, and your doctors and hospital participate in your fund’s known gap cover scheme.

However, for your hospital policy to contribute to the cost of specialist consultations (the green and yellow portion of the above example), your treatment must be as an inpatient, listed on the MBS, medically necessary and included in your hospital insurance policy with all relevant waiting periods having been served.

How can I reduce my out-of-pocket specialist costs?

Be treated by an agreement specialist

When you’re treated as a private inpatient, one of the best ways to save on out-of-pocket costs is to ask your health fund for a list of their agreement specialists for your procedure. If you can find a specialist with a no-gap agreement with your fund, you could potentially pay nothing out of pocket for your procedure.

Go to a bulk billing specialist

When you see a specialist as an outpatient for a consultation or treatment listed on the MBS, you will likely have to pay some of the cost out of pocket, unless your specialist bulk bills. When a specialist bulk bills, it means that they accept the Medicare benefit as full payment for their services, so you pay nothing. Some doctors may require you to hold a concession or health care card to be bulk billed.

Keep in mind that it can be quite difficult to find a specialist that bulk bills, depending on the specialisation and your specific healthcare needs.

Consider other costs

You may also need to pay an excess when you use your hospital policy for treatment. An excess is an amount you agree to pay when you’re admitted to hospital. If you elect to pay more for your excess, it will lower your policy premiums.

Often, you’ll only be required to pay the excess once per person per year, regardless of how many times you’re admitted to hospital. This will, however, depend on your policy and insurer.

Keep in mind that you may need to pay a co-payment instead of, or in addition to, your excess. A co-payment is where you agree to pay a certain amount for each day you’re in hospital. In some cases, the co-payment may be capped at a maximum cost per admission.

Questions to ask your insurer and specialist before treatment

When signing on the dotted line for treatment, it’s important you’re providing informed financial consent – that is, you understand and are fully aware of the costs your treatment will incur.

Below are some questions you can ask to help guide you through the process.

Ask your insurer

- Does my policy provide cover for this type of treatment?

- How much of my treatment, appointments and tests will my policy cover?

- How much will I need to pay for this treatment, including excesses and any co-payments (if applicable)?

- Which hospitals and specialists do you have agreements with?

Ask your specialist

- How much will my treatment cost, and when will I need to pay?

- Are there any other consultations or tests I may need to pay for (and when will I need to pay for them)?

- Are these costs estimates?

- Is it possible that these costs could change? If so, when will you advise me of these changes?

- Will I need to pay a gap for other specialists (e.g. anaesthetists or surgeons)?

- Will you participate in a gap cover arrangement with my health fund?

Meet our health insurance expert, Steven Spicer

As the Executive General Manager of Health, Life and Energy, Steven Spicer is a strong believer in the benefits of private cover and knows just how valuable the peace of mind that comes with cover can be. He is passionate about demystifying the health insurance industry and advocates for the benefits of comparison when it comes to saving money on your premiums.

Want to know more about health insurance?

1 Australian Department of Health: Medical doctors and specialists in Australia. Accessed January 2024.

2 Better Health Victoria: Seeing a specialist. Accessed January 2024.

Talk to an expert

At a time that suits you

Call now