Compare Private Health Insurance

Angie paid $3750 less*

Premium rises getting you down? We’ll help you compare private health insurance quotes!

*By switching from Gold to Silver+ hospital cover, increasing their excess & changing extras coverage to better suit their needs on 31/03/2026 in QLD. Reduction may change with future rate rises.

We do not compare all health funds in the market, or all policies from our partner funds. Not all policies or special offers are available to all customers, and some may only be available over the phone or on the website. Learn more.

Private health insurance offers and deals from our partners

8 weeks free

Get 8 weeks free on eligible combined hospital & extras cover (Excl. Basic Kickstarter, Basic Accident Hospital combined with Value Extras). Offer ends 31 May 2026.

Up to 8 weeks free

Get up to 8 weeks free on eligible combined hospital + extras cover. Offer ends 30 Jun 2026.

Up to 6 weeks free & 2 & 6 month waiver

Get up to 6 weeks free & 2&6-month Extras waits waived on eligible Combined Hospital & Extras Cover. Offer ends 26 Jul 2026.

4 weeks free cashback + 2 weeks donation

Get 4 weeks free cashback plus an additional 2 week premium donation. Ends 31 May 2026.

2 month waiver

Get 2-month waits waived on extras. Not available for Hospital-Only. Offer ends 30 Jun 2026.

2 & 6 month waiver

2 and 6 month waiting periods for extras waived on eligible combined hospital & extras cover (Excl. Basic Kickstarter, Basic Accident Hospital combined with Value Extras).

2 & 6 month waiver

Get 2 & 6 month waits waived on extras. Not available for Hospital-Only or Extras-Only. Offer ends 31 Aug 2026.

2 month waiver

New Members who join and commence extras only with direct debit (excl Annual) by 30 Jun 2026 will have 2-month extras waits waived, including optical. Must maintain cover for 60 days to be eligible.

2 month waiver

Get 2-month waits waived on extras. Not available for Hospital-Only or Extras-Only. Offer ends 31 Aug 2026.

Not all offers are available to every customer, and some offers may only be available through our contact centre and not displayed online. Each offer is subject to the provider’s terms and conditions. Learn more about how offers are displayed or call us on 1800 338 253 for more information.

Premiums going up? Our customers are paying less

Angie lowered their annual premium by

0

By switching from Gold to Silver+ hospital cover, increasing their excess & changing extras coverage to better suit their needs on 31/03/2026 in QLD. Reduction may change with future rate rises.

Shane and Alex lowered their annual premium by

0

By switching their Silver hospital (with extras) cover to Bronze+ hospital cover & changing extras coverage to better suit their needs on 31/03/2026 in QLD. Reduction may change with future rate rises.

Jacques lowered their annual premium by

0

By switching from Silver+ to Silver hospital cover & reducing extras coverage to better suit their needs on 15/11/2025 in QLD. Reduction may change with future rate rises.

Mark lowered their annual premium by

0

By switching from Silver+ to Silver hospital cover & reducing extras coverage to better suit their needs on 12/05/2025 in VIC. Reduction may change with future rate rises

What are the different types of health insurance?

We’ve compiled this table to show the different types of health insurance and what services each one covers. This information should be used as a guide only and you should always check policy documents for specific details.

We won't be beaten on price

Buy health insurance with us, and if you find the same policy cheaper elsewhere, we’ll give you 110% of the difference for the first year. Learn more. T&Cs apply.

Top 5 things to know about health insurance

It pays to compare health insurance

Compare personalised health insurance quotes in minutes and start saving today.

Simple to use

Get started by answering a few quick questions to help us understand your health insurance needs.

Compare & save

Save time and money by easily comparing health insurance options from a range of providers side-by-side.

Switching is easy

Follow a few easy steps online to switch to a new health insurance policy that suits you and your budget.

Why compare with us?

Our smart comparison technology is trusted, free, safe and secure.

We believe the best decisions start with a comparison.

We’re proud to have helped millions of Aussies look for a better deal.

4.3 / 5

Based on 3,166 reviews

23 million comparisons and counting

4.7 / 5

Based on 2,377 reviews

Ratings as of 30/03/2026.

A guide to health insurance

Updated 26 March 2026

Dr Ginni Mansberg explains the benefits of having private health insurance

Ginni Mansberg

Health insurance expert

Transcript

Hi, it’s Dr. Ginni Mansberg, GP and health commentator in the media. Today we’re talking about why you might need private health insurance. Australia is lucky enough to have an excellent medical system that helps you access healthcare for many medical problems.

At the same time, the federal government strongly encourages those who can to take out private health insurance as well. If you don’t have private health insurance and you earn above a certain threshold, you’ll pay a Medicare Levy Surcharge on your tax return. On the other hand, the government offers rebates on the premiums for some of us who do take out private health insurance. Your private health insurance is there in case you need it.

It’s there for those events that most of us don’t see coming. A tooth extraction, a busted knee or radiotherapy for cancer in an emergency, you’re covered through the public system. But if you need access to allied health professionals, reduced waiting times for surgery or you want treatment in a private hospital, having private health insurance could be really beneficial for you and your family. In Australia, There are over 30 insurers offering over 3,000 different health insurance products and it pays to shop around before you jump in.

Health insurance is not a one size fits all solution, and it’s worth getting some help to find the policy that’s right for you. Chat to the experts about whether private health insurance is a good option for you. And which one best suits your needs.

Premiums, charges and tax breaks

Of those we surveyed for our 2025 Household Budget Barometer report, the average Aussie spends $255.67 per month on health insurance, or $3,068.04 annually.1 However, this should be taken as a guide as many factors can influence your health insurance costs.

Below is what the average Australian’s monthly health insurance premiums by state:1

How much is the health insurance premium increase in 2026?

The health insurance premium increase will be an industry average of 4.41% and will occur from 1 April 2026. However, depending on your specific health fund or policy, you may experience a higher or lower premium rise, or your policy price may even stay the same.

All policyholders need to know what their premium adjustment will be, as it’ll help them prepare financially and decide whether their current policy still suits their needs. The below table offers an insight into how premium rises can affect your total costs, based on the industry average.2

| Potential premium adjustments | ||

|---|---|---|

| Policy type | Average policy cost * | +4.41% |

| Hospital cover | $2,641 | $116 |

| Extras cover | $839 | $37 |

| Hospital and extras cover | $3,560 | $156 |

| *Average based on all private health insurance policies purchased via Compare the Market between 1 January and 30 November 2025. These figures include rebates and age-based discounts as well as lifetime health cover loading where applicable. | ||

Worried about how the rate rise will affect your premiums? Many policyholders manage to save money by either prepaying their annual premiums before 1 April or switching to another policy that offers a better deal. Compare today through our free online comparison tool or give us a call to chat to one of our friendly team-members at our Brisbane-based contact centre.

What’s the average rate rise per fund?

The below table shows the average rate rise for each health fund in 2026. Remember, these are the overall averages of all policies offered by each fund, meaning your policy may experience a different premium adjustment.

| Health fund | Average 2026 rate rise |

|---|---|

| ACA Health Benefits Fund Limited | 4.48% |

| AIA Health Insurance | 5.98% |

| Australian Unity Health Limited | 3.98% |

| BUPA HI Pty Ltd | 4.80% |

| CBHS Corporate Health Pty Ltd | 3.25% |

| CBHS Health Fund Limited | 3.25% |

| Defence Health Limited | 2.99% |

| Doctors’ Health Fund Pty Ltd | 3.67% |

| GMHBA Limited | 1.98% |

| HBF Health Limited | 2.15% |

| Health Care Insurance Ltd | 4.53% |

| Health Insurance Fund of Australia Limited | 2.60% |

| Health Partners Limited | 3.94% |

| Hospitals Contribution Fund of Australia Ltd | 4.96% |

| Hunter Health Insurance* | 3.92% |

| Latrobe Health Services Limited | 4.53% |

| Medibank Private Limited (AHM) | 5.10% |

| Mildura District Hospital Fund Ltd | 4.25% |

| National Health Benefits Australia Pty Ltd | 2.96% |

| Navy Health Ltd | 2.88% |

| NIB Health Funds Ltd | 5.47% |

| Peoplecare Health Limited | 4.01% |

| Phoenix Health Fund Limited | 2.95% |

| Police Health Limited | 2.53% |

| Reserve Bank Health Society Ltd | 4.13% |

| St Luke’s Medical and Hospital Benefits Association | 4.25% |

| Teachers Federation Health Ltd | 3.94% |

| Westfund Limited | 3.26% |

|

Source: health.gov.au |

|

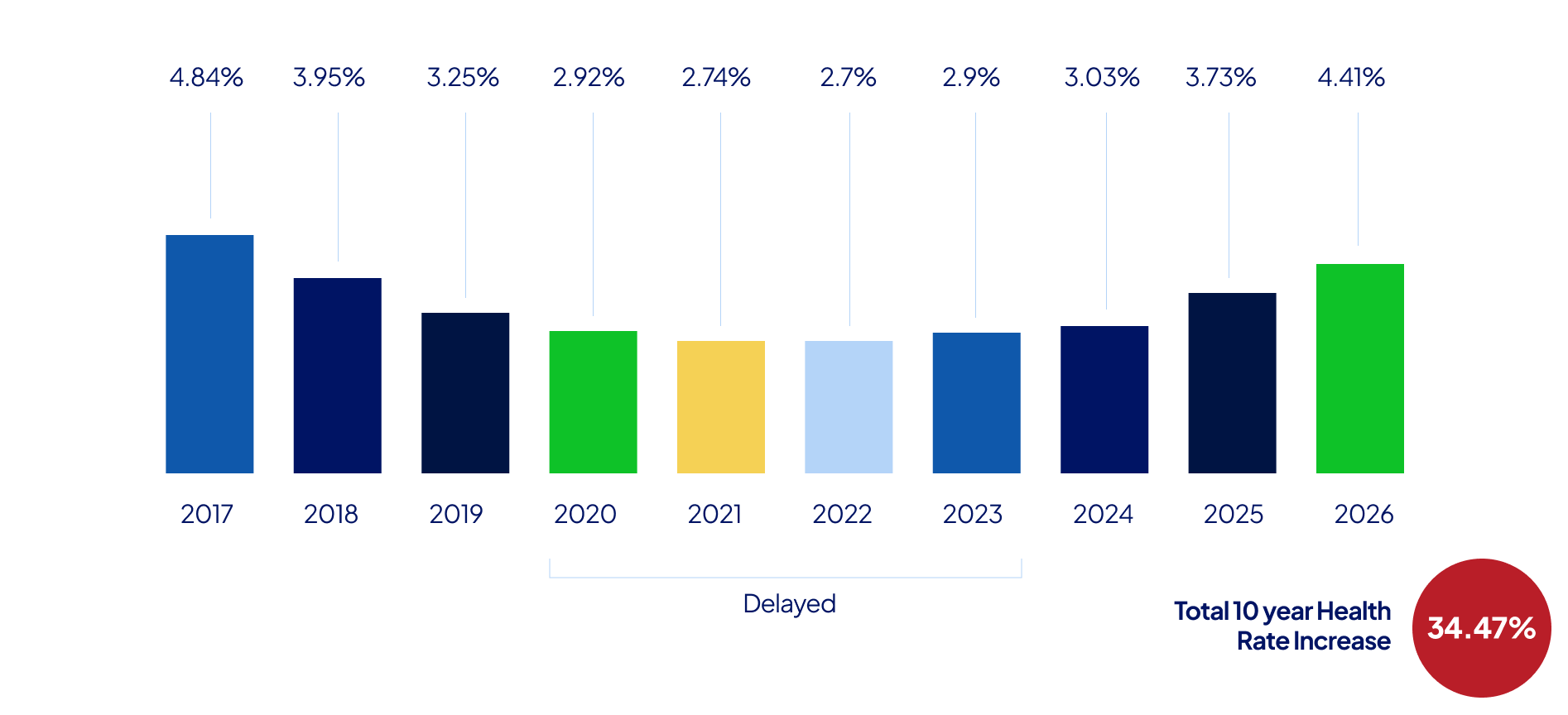

Do premiums increase over time?

Over the last decade, the industry average for health insurance premiums has risen every single year, which can greatly increase the cost of existing policies.1 The graph below shows the health industry rate increase by year for the last decade:

Some of the key reasons for these consistent premium rises include:

- Increase in doctor/specialist fees

- Rising treatment and service costs

- Higher costs for medical equipment

- Wage increases for healthcare workers

In general, premiums for specific policies with different health funds increases from 1 April annually, although this did fluxuate a little during the COVID-19 pandemic.

How much does health insurance cost?

The cost of private health insurance in Australia depends on:

- The type of policy

- Your level or cover or tier

- The state or territory where you live

- The rebates and discounts you receive based on your age or income

- Your Lifetime Health Cover loading (LHC).

Private health insurance in Australia is community rated, meaning that you’ll never be charged a higher base premium than someone else for the same policy based on risk factors such as age, race, gender, pre-existing conditions or any other reason. However, several factors can still affect how much you pay in premiums or for premium increases, such as your level of cover, state of residence, rebates, discounts and LHC loading.

For hospital cover, policies are divided into four tiers (Basic, Bronze, Silver and Gold) which are priced accordingly. Taking out a higher level of hospital cover will naturally cost you more, although you can often reduce your premiums by agreeing to a higher excess instead. Extras cover levels are decided by the insurer and aren’t regulated by the government like hospital cover is.

How to get cheaper health insurance

Your premiums will also be influenced by your eligibility for an age-based discount, the Australian Government’s rebate and if a Lifetime health cover (LHC) loading applies.

- Age-based discount. Some insurers will offer an age-based discount of up to 10% if you take out a policy before you turn 26. The discount you may be entitled to is reduced by 2% for each year after the age of 25 that you don’t take out a policy. By holding continuous hospital cover with a policy that lets you retain your aged-based discount, you can enjoy the discount until the age of 41. From the age of 41, the discount is phased out by 2% each year until it reaches zero.

- Government rebate. If you qualify, the Australian Government’s private health insurance rebate helps reduce the cost of your premiums depending on your age and income. For example, if you qualify for the highest tier of the rebate, you can potentially receive a premium refund of 32.158%.

- LHC loading. If you don’t take out hospital insurance before the 1st of July following your 31st birthday, you may have to pay an increased premium due to the LHC loading. This is to encourage Australians to take out a hospital insurance policy earlier in life to reduce the strain on the public system.

Shopping around and comparing your policy annually can also help you reduce your health insurance premiums. Of those we surveyed, those who have been with the same provider for a single year pay an average of $237.84 in monthly premiums.1 Those who’ve remained with the same health fund for over a decade pay an average of $306.88 per month, 29% more than those who switched to a new fund.

Is private health insurance tax deductible?

While not tax deductible, private health insurance can still have an impact on your tax.

The private health insurance rebate is available to anyone who holds an eligible Medicare card and falls within the set income thresholds with a hospital or combined hospital and extras health insurance policy. It can be claimed each year via your tax return. Alternatively, you can also choose to claim the rebate as a discount on your premiums instead.

Also, if you earn more than $101,000 as a single or $202,000 as a couple or family and don’t hold sufficient private hospital insurance, you could incur the Medicare Levy Surcharge (MLS). The MLS is a government surcharge added onto the taxable income of high-income earners who don’t hold private hospital cover. It is applied as a percentage of your annual income (e.g. 1-1.5%), which you’ll need to pay for the number of days in the financial year that you and your family didn’t hold suitable hospital coverage.

What is a health insurance excess?

When you’re admitted to hospital as a private patient, you may have to pay a lump sum to your private health insurer, which is known as the excess. This could be in the form of a payment per hospital admission, but may only be for the first admission of the calendar, financial or membership year per person, depending on your insurance provider and policy. Choosing a higher excess may allow you to pay lower premiums.

You may also have to pay a co-payment, which is a set amount you’re required to pay each day you’re in the hospital. This is typically capped per hospital stay.

What does ‘no gap’ mean in health insurance?

Each eligible hospital treatment has a Medicare Benefits Schedule (MBS) fee, a price the government believes is fair. Medicare pays 75% of this fee, while your health insurer pays the remaining 25%.

If your specialist charges above this fee, you may have to pay the extra amount not covered by Medicare and your private health insurance. Alternatively, your health fund may pay some or all of this gap.

For extras services, gap cover simply means that the health care provider doesn’t charge above your extras benefits limit and rebate, which results in no out-of-pocket costs.

Your insurer may have agreements with certain providers to eliminate or minimise out-of-pocket expenses. Be sure to check with your insurer before seeking treatment to understand what costs you may incur.

For more information, check out our page explaining gap payments.

Expert tips for comparing health insurance online

Our health insurance expert, Steven Spicer, has some helpful tips for finding the right health insurance policy for you.

Steven Spicer

Executive General Manager – Health, Life & Energy

Flexibility is key

Flexibility is one of the key benefits of private health insurance. For example, any waiting periods that you have already served will be recognised by your new fund if you switch to the same or lower level of cover.

Buy for your current needs

When selecting your coverage, it’s a good idea to consider what you might need to include on your policy right now or in the near future. The great thing about health insurance is you can upgrade at any time, just keep in mind that you may need to serve a waiting period for any upgrades. In hospital cover, most waiting periods are only 2 months, excluding pregnancy and birth and most pre-existing conditions which will incur a 12-month waiting period

Get the right level of cover

Deciding on the right level of cover can be vital. It could mean the difference between being covered or leaving yourself out of pocket. Some choose to take out hospital cover alone, while others consider extras only, or a combination of the two.

Find out more about health insurance

What is private health insurance?

In Australia, private health insurance (PHI) helps cover healthcare costs not fully covered by Medicare, up to the limits of your policy.

Private health insurance supplements, rather than replaces, Medicare, so you’ll still have access to public healthcare even if you have private insurance.

There are two types of private health insurance:

- Hospital cover: This pays a benefit towards medically necessary treatment as a private patient in a public or private hospital.

- Extras cover (also known as general treatment or ancillary cover): This can help cover the cost of many out-of-hospital medical treatments, such as physiotherapy, optical, and dental care.

Along with paying towards the cost of private health care, private hospital cover often offers a wider choice of doctors and hospitals than the public health system, as well as shorter wait times for elective surgeries.

To benefit from both types of cover, you can take out a combined cover policy. Whatever type of cover you choose, you’ll need to pay ongoing fees (premiums) to keep your policy active.

If you’re a high-income earner (single earning over $101,000 or a couple/family earning over $202,000) and don’t have private hospital cover, you’ll have to pay the Medicare Levy Surcharge (MLS). This is an additional tax of between 1-1.5%, depending on your income.

When taking out a new policy or upgrading your current cover, you may need to serve a waiting period before you can make a claim.

Why should I take out private health insurance?

You might want to consider private health insurance if you value having more choice when it comes to your healthcare, such as:

- Avoiding public waiting lists for elective surgeries. When you’re treated through the private system, you may be able to avoid often lengthy public hospital waiting lists by being treated in a private hospital. Once you’ve served your waiting periods, you could receive treatment in a matter of days or weeks. The waiting period will depend on the procedure, as well as the availability of the treating doctor and hospital.

- Choosing your own doctor and stay in a private room. Depending on availability, you may be able to choose your own treating doctor and recover in a private room when you’re admitted to a private hospital.

- Getting cover for out-of-hospital treatment. With an extras cover policy, you can claim benefits for some out-of-hospital treatments that Medicare doesn’t cover. This includes services like dental, physio and chiro.

How does private health insurance work in Australia?

In Australia, there is a hybrid healthcare system that combines Medicare, which is a public healthcare system that provides free or subsidised treatment, and private health insurance, which is optional and allows you to choose your own available doctor and hospital. Extras cover also helps cover the cost of out-of-hospital services that Medicare doesn’t cover, such as dental and optical.

Private health insurance can be purchased in a few different forms. Private hospital cover gives you the option of being treated in hospital as a private patient, so you can choose your own available doctor, stay in a private room (when available) and potentially avoid long public hospital waiting lists, among other perks. Hospital cover is available in four tiers: Basic, Bronze, Silver and Gold. Your hospital cover, in combination with Medicare, will cover you for 100% of the Medicare Benefit Schedule (MBS) fee if you are admitted to hospital as a private patient. You may still have a gap payment, which is the difference between the MBS fee and the cost of your medical treatment if your doctor or surgeon charges above the MBS fee.

If you had a medical issue before taking out your hospital policy, it may be considered a pre-existing condition. Luckily, you won’t have to pay any more for your policy than someone without a medical history would, but you may have to serve up to a 12-month wait before you can claim on any relevant treatments.

Extras cover helps pay for many out-of-hospital treatments that Medicare does not cover, like dental, physiotherapy and optical. For extras services, your insurance provider will pay either a percentage of the total cost or a set dollar amount. The amount you can claim may be subject to limits, such as lifetime, annual or sub limits.

Some government incentives and surcharges can affect your health insurance premiums. These are:

- Private Health Insurance Rebate: An income and age-tested government rebate to help cover the costs of health insurance premiums.

- Lifetime Health Cover (LHC) Loading: A government initiative designed to encourage Australians to take out hospital cover sooner. If you take out hospital cover for the first time later in life, there will be a 2% loading to your premiums for each year you are aged over 30.

- Medicare Levy Surcharge: If you’re a high-income earner (earning over $101,000 or earning over $202,000 as a couple/family), you’ll have to pay an additional 1-1.5% tax if you don’t have private hospital cover.

Always check your policy brochure before making a claim, as limits, exclusions, and waiting periods apply.

Levels of cover

For hospital cover, there are four tiers of cover: Basic, Bronze, Silver and Gold. The following is the minimum clinical categories each tier must include:

- Basic: 3 restricted clinical categories

- Bronze: 18 clinical categories and 3 restricted clinical categories

- Silver: 26 clinical categories and 3 restricted clinical categories

- Gold: 38 clinical categories

Though health funds are required to meet the minimum requirements of each tier, they can also add additional clinical categories through what’s known as ‘Plus’ products. For example, a Silver-plus policy could include a clinical category that’s usually only included in Gold tier, such as joint replacement. This could potentially allow you to get the cover you need without paying the higher premium of a higher tier.

Extras cover is also often available in different levels of cover. However, unlike hospital cover, there aren’t government-mandated minimum requirements for extras cover. This means health funds can create their own levels of cover and what these levels include.

What does private health insurance cover that Medicare doesn’t?

The public and private healthcare systems complement each other. When you have hospital cover and are treated in a private hospital, both Medicare and your health fund can contribute to the cost. When you have extras cover, your health fund helps you pay for out-of-hospital services that aren’t covered by Medicare, such as dental, optical and physio.

If you’re admitted to a private hospital as a private patient, Medicare will pay 75% of the Medicare Benefits Schedule (MBS) fee for your procedure. Your private health insurance pays the other 25%, as well as contributing towards accommodation costs and theatre fees. There may be a ‘gap’ between the MBS fee and the total cost of your procedure. You may have to pay this gap, or your health fund may cover some or all of it.

Extras cover

Extras cover helps you pay for services that aren’t covered by Medicare, like dental treatment and physiotherapy. In some areas, such as optical treatment, Medicare and private health insurance work together. Medicare can pay for your eye check and consultation with the optometrist, while your private health insurance helps you pay for your prescription glasses or contact lenses.

Pregnancy

Cover for pregnancy and birth-related services is included in Gold hospital insurance policies and some ‘plus’ policies (like Silver Plus). Hospital cover for pregnancy and birth has a 12-month waiting period, so you need to have it before you get pregnant.

Private hospital insurance with pregnancy cover can help you to pay for:

- Private inpatient pregnancy admissions

- Labour and post-natal care

- C-sections

- In-patient obstetrician care

- A private hospital room (if it’s available).

Some private hospital policies also cover assisted reproduction services, such as infertility testing, in-vitro fertilisation (IVF) and gamete intro-fallopian transfer (GIFT). However, hospital insurance only pays a benefit towards in-patient care (i.e. the treatment you receive as a patient admitted in the hospital).

Dental

Dental cover is usually only available through extras cover, but private hospital policies can help pay for dental treatment and operations you have in hospital. What’s covered by your policy depends on your level of cover, but generally dental check-ups are standard.

Your health insurance provider will usually set annual limits on how much you can claim for dental. You can check this in your policy documents.

Optical

Optical services and products can be included on either hospital or extras policies, depending on your needs. Treatments you get in hospital will come under hospital cover, while extras cover can help pay for eyewear.

Other medical and allied health services

Depending on your policy, your extras health insurance might help you pay for other services such as:

- Psychology services

- Physiotherapy

- Gym memberships

- Remedial massages

- Occupational therapy

- Hearing devices and audiology

- Podiatry

- Sleep studies

- Dieticians

- Chiropractic services

- Natural remedies.

When looking at potential policies, consider which services you’ll need and likely use. Knowing which services you want will help you determine the right level of cover for your needs.

What is private health insurance comparison?

Private health care comparison is the process of comparing different providers and policies and evaluating which is the best fit for your health needs, lifestyle and budget. Some key factors to keep in mind when comparing include:

- The type of cover you’ll need (e.g. hospital, extras or combined)

- Level of cover you need

- Waiting periods you may need to serve

- Benefits

- Policy exclusions

Comparing policies allows you to see what options are on the market and can help you find a policy that better suits your needs. Research shows that 58% of health insurance customers in Australia have remained with the same health fund for five years or more.1 By not shopping around, they’re potentially paying a “loyalty tax” and missing out on better deals elsewhere.

Which is the best health insurance for me?

The best fund for you depends on your unique circumstances. Thanks to our handy private health insurance comparison service, we make it even easier to find health insurance. With our free tool, it takes only minutes to compare policies side-by-side to find great-value cover that suits your family’s needs. Our partner funds are:

We do not compare all health funds in the market, or all policies from our partner funds, and at times certain funds or products might be unavailable. Learn more.

Private health insurers in Australia

Below is a list of all registered health funds in Australia. Policies are sometimes sold under secondary brand names or by another company, which aren’t included in this list.

- ACA Health Benefits Fund

- ahm health insurance

- AIA Health Insurance Pty Ltd

- Australian Unity Health Limited

- Bupa HI Pty Ltd

- CBHS Corporate Health Pty Ltd

- CBHS Health Fund Limited

- CDH Benefits Fund

- CUA Health

- Defence Health Limited

- Doctors’ Health Fund

- GMHBA Limited

- GU Health

- HBF Health Limited

- HCF

- HCi

- Health Insurance Fund of Australia Limited

- Health Partners

- Latrobe Health Services

- Medibank Private Limited

- Mildura Health Fund

- National Health Benefits Australia Pty Ltd (onemedifund)

- Navy Health Ltd

- nib Health Funds Ltd

- Peoplecare Health Insurance

- Phoenix Health Fund Limited

- Police Health

- Queensland Country Health Fund Ltd

- Reserve Bank Health Society Ltd

- rt health – a division of The Hospitals Contribution Fund

- St.Lukes Health

- Teachers Health

- TUH Health Fund

- Westfund Limited

The information provided is current as of August 2025 and sourced from the Private Health Insurance Ombudsman. This list is subject to change.

Private health insurance waiting periods

If it’s the first time you’re taking out health insurance or you’re upgrading your policy, you’ll typically need to serve a waiting period before you can make a claim. The length of this waiting period will depend on the clinical category or inclusion.

The good news is that if you’re switching to a policy with the same or lower coverage, you won’t have to re-serve any waiting periods you’ve already completed. If you’re upgrading your policy, you’ll only have to serve waiting periods for additional inclusions you didn’t have in your previous policy.

Waiting periods for hospital cover

Waiting periods for hospital cover are regulated by the government and are standard across the industry. If you have a pre-existing condition, it’ll extend the length of your waiting period for many clinical categories (usually from 2 months to 12 months). The table below offers an outline of typical waiting periods for hospital cover:

| Service | Waiting period |

|---|---|

| Treatments for pre-existing health conditions | 12 months |

| Birth-related services and pregnancy | 12 months |

| Rehabilitation, palliative care and psychiatric care (even for a pre-existing condition) | 2 months |

| All other conditions | 2 months |

Being aware of waiting periods allows you the chance to plan ahead. For example, if you’re planning on having children, you can take out a Gold-level policy 12 months before birth, so you’ll have the peace of mind that you’ll be covered in-hospital during delivery.

Waiting periods for extras cover

Unlike hospital cover, waiting periods for extras cover are not standardised and are decided by the health funds themselves. These waiting periods can vary from 0-2 months for services like dental and physio to 12 months for more expensive services such as major dental.

While extras cover waiting periods can vary, the table below provides some typical waiting times for some inclusions.

| 2 months | 6 months | 12 months | 1, 2 or 3 years |

|---|---|---|---|

| Physiotherapy and general dental | Optometry (e.g. glasses) | Major dental procedures, like crowns | Orthodontics and other high-cost procedures |

Sometimes, health funds may waive waiting periods on some inclusions as a promotion to attract new members, so it’s worth keeping an eye out for these offers. Usually, waiting periods will only be waived for inclusions with a shorter waiting period. A promotion is unlikely to waive a 12-month waiting period for an inclusion like major dental.

Ambulance cover

Medicare doesn’t pay for ambulance services. You can get cover for ambulances from some private health insurers, and people in Queensland and Tasmania have ambulance services covered by their state governments, you are covered throughout Australia.

Some ambulance services offer memberships to cover the costs of transport and treatment. Many health funds offer ambulance cover that you can buy on its own, or there may be some ambulance cover included on your health insurance policy.

Even if you’re covered in your own state, this may not apply when you travel interstate. To avoid out-of-pocket ambulance costs while travelling interstate, residents in all states or territories (except for Queensland) may need private health insurance with nationwide ambulance cover or a domestic travel insurance policy.

The table below outlines how ambulance services are covered across Australia.

| NSW |

The NSW state government subsidises 49% of the cost of ambulance services for people who don’t have ambulance cover. Otherwise, ambulance cover is widely available through registered Australian health funds in NSW. NSW residents with a Health Care Card, Pensioner Concession Card, Commonwealth Seniors Health Care Card and who otherwise meet NSW’s exemption criteria can access ambulance services at no cost |

| VIC |

Residents of VIC can take out ambulance cover through a registered Australian health fund or a subscription from the state ambulance service. VIC residents who hold a Pensioner Concession Card or Healthcare Card are entitled to free ambulance cover. |

| QLD |

The QLD state government covers ambulance services for their residents in both QLD and around Australia. If you receive a bill for ambulance services in another state or territory, you can forward it, along with proof of QLD residency, to the Queensland Ambulance Service. |

| WA |

Residents of WA can take out ambulance cover through a registered Australian health fund or a subscription from the state ambulance service. WA residents who are aged Pensioner concession holders may be entitled to free ambulance transport services. Western Australians over 65, and in receipt of an Australian Government pension, are entitled to free ambulance services. Western Australians over 65, who do not receive an Australian Government pension, are entitled to a 50% discount off the cost of ambulance service. |

| SA |

Residents of SA can take out ambulance cover through a registered Australian health fund or a subscription from the state ambulance service. |

| TAS |

Ambulance services in TAS are free for residents, except for motor vehicle or workplace accidents, which are covered by state insurance. Unlike QLD, Tasmanians can only receive free ambulance cover in their state. Therefore, Tasmanians should consider taking out nationwide ambulance cover or buy travel insurance before travelling interstate. |

| ACT |

Residents of the ACT can take out ambulance cover through a registered Australian health fund. People who meet the ACT Ambulance Service’s exemption criteria (including Pensioner Concession Card and Healthcare Card holders) are entitled to free ambulance services. |

| NT |

Residents of NT can take out ambulance cover through a registered Australian health fund or a subscription from the state ambulance service. NT residents who are Pensioner Concession Card or Health Care Card holders are entitled to free ambulance cover. |

The cost for Australia’s top surgeries

When you receive an elective surgery included on your hospital insurance policy as a private inpatient, Medicare will pay 75% of the Medicare benefit schedule (MBS) fee for the cost of your procedure. Your private hospital insurance will pay the remaining 25%.

Because private specialists are allowed to set their own fees, there may be a difference between the MBS fee and the actual cost you end up being charged, known as the ‘gap’. Depending on your policy and treating doctors, this gap may be partially or fully paid by your health fund through their gap cover scheme.

There are also various hospital fees associated with private treatment, such as accommodation, theatre fees, and medical devices. These hospital fees can get quite expensive; luckily, your health insurance can also cover some or all of these fees, although you may have to pay an excess or co-payment.

Any fees that aren’t covered by Medicare or your health fund will need to be paid by the patient. It’s a good idea to speak to your treating doctors and health fund prior to receiving treatment to understand any potential out-of-pocket costs.

Below are some of Australia’s most common elective surgeries3 and their typical costs in a private setting with private health coverage. Keep in mind that these are a general guide only and your own personal costs will vary.

The cost for Australia’s top surgeries

Cataract surgery

- The typical specialists’ fee for cataract extraction was $2,1004

- 42% of patients had no out-of-pocket costs

- Those with an out-of-pocket cost typically paid $480

- The typical hospital fee for this procedure was $2,500

Cystoscopy with biopsy

- The typical specialists’ fee for a cystoscopy with biopsy was $1,2005

- 27% of patients had no out-of-pocket costs

- Those with an out-of-pocket cost typically paid $350

- The typical hospital fee for this procedure was $1,400

Cholecystectomy

- The typical specialists’ fee for a cholecystectomy was $3,1006

- 19% of patients had no out-of-pocket costs

- Those with an out-of-pocket cost typically paid $500

- The typical hospital fee for this procedure was $4,700

Total knee replacement (single)

- The typical specialists’ fee for a total knee replacement was $5,2007

- 18% of patients had no out-of-pocket costs

- Those with an out-of-pocket cost typically paid $1,000

- The typical hospital fee for this procedure was $18,000

Femoral or inguinal herniorrhaphy

- The typical specialists’ fee for an inguinal herniorrhaphy was $2,2008

- 27% of patients had no out-of-pocket costs for their doctors

- Those with an out-of-pocket cost typically paid $500

- The typical hospital fee for this procedure was $3,900

Total hip replacement (single)

- The typical specialists’ fee for a total hip replacement was $5,6009

- 16% of patients had no out-of-pocket costs

- Those with an out-of-pocket cost typically paid $1000

- The typical hospital fee for this procedure was $20,000

Abdominal hysterectomy

- The typical specialists’ fee for an abdominal hysterectomy was $3,10010

- 20% of patients had no out-of-pocket costs

- Those with an out-of-pocket cost typically paid $670

- The typical hospital fee for this procedure was $7,200

Total prostatectomy

- The typical specialists’ fee for a total prostatectomy was $9,80011

- 4% of patients had no out-of-pocket costs

- Those with an out-of-pocket cost typically paid $6,000

- The typical hospital fee for this procedure was $12,000

Septoplasty

- The typical specialists’ fee for septoplasty was $2,50012

- 23% of patients had no out-of-pocket costs

- Those with an out-of-pocket cost typically paid $650

- The typical hospital fee for this procedure was $2,500

Myringotomy

- The typical specialists’ fee for a myringotomy was $1,60013

- 16% of patients had no out-of-pocket costs

- Those with an out-of-pocket cost typically paid $520

- The typical hospital fee for this procedure was $1,300

Why compare health insurance online?

With so many health insurance providers and policies available, it can be hard to know which one is right for you. In fact, over a third of Australians say they’ve been with the same provider for over a decade, meaning they’re potentially missing out lower premiums elsewhere.1

Compare the Market can help you on your journey to find the best health insurance for you. You can compare health insurance through our free comparison service in minutes, or if you prefer a more personal approach, you can talk to someone at our expert run, Brisbane-based contact centre to discuss your options.

Meet our health insurance expert, Steven Spicer

As the Executive General Manager of Health, Life and Energy, Steven Spicer is a strong believer in the benefits of private cover and knows just how valuable the peace of mind that comes with cover can be. He is passionate about demystifying the health insurance industry and advocates for the benefits of comparison when it comes to saving money on your premiums.

Steven has 20 years of experience as a people-first business leader, with a focus on creating services that put customers first.

1 Compare the Market – Household Budget Barometer 2025. Accessed October 2025.

2 Compare the Market – What a 4-5% health insurance hike could mean for your wallet. Accessed January 2026

3 Australian Institute of Health and Welfare – Elective surgery waiting times, 2022-23. Accessed September 2024

4 Australian Department of Health and Aged Care – Medical Cost Finder – Cataract Surgery, 202-22. Accessed August 2025

5 Australian Department of Health and Aged Care – Medical Cost Finder – Cystoscopy with biopsy (examine bladder). Accessed August 2025

6 Australian Department of Health and Aged Care – Medical Cost Finder – Cholecystectomy. Accessed August 2025

7 Australian Department of Health and Aged Care – Medical Cost Finder – Total knee replacement. Accessed August 2025

8 Australian Department of Health and Aged Care – Medical Cost Finder – Femoral or inguinal hernia repair. Accessed August 2025

9 Australian Department of Health and Aged Care – Medical Cost Finder – Hip Replacement. Accessed August 2025

10 Australian Department of Health and Aged Care – Medical Cost Finder – Open abdominal hysterectomy. Accessed 2025

11 Australian Department of Health and Aged Care – Medical Cost Finder – Total prostatectomy. Accessed 2025

12 Australian Department of Health and Aged Care – Medical Cost Finder – Septoplasty. Accessed 2025

13 Australian Department of Health and Aged Care – Medical Cost Finder – Grommets/myringotomy. Accessed 2025.

Methodology of how the offers are displayed

Offers are displayed in the following order and preference:

- Weeks Free

- Cashback / Gift Card

- Waiting Period Waiver

- Cover Type

- Offer Expiry

- Alphabetical

Offer terms and conditions

Join and commence your Australian Unity policy by 30 June 2026 and get up to 8 weeks free on eligible hospital and extras cover. Excludes Extras and Hospital-Only. Must not have held Australian Unity health insurance within 90 days prior to joining. Must complete 60 days of continuous paid membership, with no suspension or arrears, before being eligible for initial 6 weeks free, and need to complete 365 days of continuous paid membership on eligible cover to receive the additional 2 weeks free. Offer fulfilled by extending paid-to date and can take up to 90 days from joining date for the weeks free to be applied provided payment has been maintained during this time. See full terms and conditions here.

Offer terms and conditions

For new members who have not been a GMHBA member in the last 12 months, pay on direct debit. Must pay first month to start claiming. 12 month waits, annual and sub limits apply. Extras claims made with a previous fund count towards your annual limits. Not available with any other offer. Offer valid from 1 October 2025 to 31 August 2026.

Offer terms and conditions

New members that take out & commence combined or extras only cover with HCF by 30 June will have the 2-month extras waits waived. Extras waits that are longer than 2 months and all waiting periods for hospital treatments still apply. Must not have been insured under and RT Health or HCF health policy in the 2 months prior to taking out the offer, or have received any promotional discount from RT Health or HCF in the 12 months prior. See full terms and conditions here.

Offer terms and conditions

For new members who have not been a Frank member in the last 12 months, pay on direct debit. Must pay first month to start claiming. 12 month waits, annual and sub limits apply. Extras claims made with a previous fund count towards your annual limits. Not available with any other offer. Offer valid from 17 February 2026 to 31 August 2026.

Offer terms and conditions

New HIF Members who join and commence eligible extras only cover with HIF and pay by direct debit (excl annual payments) by 30 June 2026 will have the 2-month extras waits waived, including optical, which means you can start claiming on any available limits and benefits straight away. Must maintain cover for 60 days to remain eligible, or hif may withhold the claim value from the premium refund. If the premium refund does not cover the full cost, the member may be required to reimburse the remainder. See full terms and conditions here.

Offer terms and conditions

Join see‑u by HBF by 26 July 2026 on an eligible combined Hospital & Extras cover and get up to 6 weeks free plus 2&6‑month Extras waiting periods waived. Excludes Hospital‑only, Extras‑only, employees, existing see‑u members, and anyone who has received a see‑u promotional joining offer in the past 18 months. Must complete 8 weeks of continuous paid cover to receive the initial 4 weeks free, and 12 months of continuous paid cover to receive the additional 2 weeks free at month 13. Free weeks are applied by extending the paid‑to date; direct debits pause automatically during free‑cover periods. Member must be financial and have paid 4 weeks of premiums before any claims can be approved. Eligible claims for services received from the join date will be payable once this is met. Hospital waits and Extras waits over 6 months still apply. See full terms and conditions here.

Offer terms and conditions

Join and commence an eligible nib combined Hospital and Extras policy by 31 May 2026 and receive 8 weeks free. Policy must remain active with premiums up to date until the offer is applied on 29 July 2026. Weeks free are applied as a paid‑to‑date extension. Excludes Extras‑only, Hospital‑only and ineligible products including Basic Kickstarter and Basic Accident Hospital combined with Value Extras, non‑health insurance products, current nib members or partner brands, and anyone who has held these products in the past 6 months.

*Product issued by nib include: Qantas Health Insurance, Suncorp Health Insurance, GU Health Insurance, AAMI Health Insurance, Apia Health Insurance, ING, Real Health Insurance, Seniors Health Insurance, nib International Workers Health Insurance, nib Overseas Students Health Insurance or nib Corporate Health Insurance. Eligible members who join an Eligible product during the Offer period, which has a start date outside of the Offer Period can qualify for the offer subject to their compliance with NIB’s terms and conditions. See full terms and conditions here.

Offer terms and conditions

Join and commence an eligible nib combined Hospital and Extras policy by 31 May 2026 and receive 2 & 6‑month waiting periods waived on eligible extras. Applies from the policy start date once the first premium is paid. Excludes Extras‑only, Hospital‑only and ineligible products including Basic Kickstarter and Basic Accident Hospital combined with Value Extras, non‑health insurance products, current nib members or partner brands, and anyone who has held these products in the past 6 months.

*Product issued by nib include: Qantas Health Insurance, Suncorp Health Insurance, GU Health Insurance, AAMI Health Insurance, Apia Health Insurance, ING, Real Health Insurance, Seniors Health Insurance, nib International Workers Health Insurance, nib Overseas Students Health Insurance or nib Corporate Health Insurance. Eligible members who join an Eligible product during the Offer period, which has a start date outside of the Offer Period can qualify for the offer subject to their compliance with NIB’s terms and conditions. See full terms and conditions here.

Offer terms and conditions

Join & commence an Eligible AIA Health Hospital or combined Hospital & Extras policy by 31 May 2026 and maintain continuous paid membership until 7 September 2026 will receive 4 weeks free as a premium cashback. AIA Health will also make a one‑off donation equivalent to 2 weeks’ premium, based on the policy held at the end of the qualifying period, to the Mother’s Day Classic Foundation. Cashback is paid within 30 business days after the Qualifying Period. Eligible members have not held and have not been insured under an AIA health insurance policy in the two months prior to 1 May 2026 or have used any discount issued by AIA in the last 12 months.

*Eligible Policy must not be in arrears, terminated or suspended within any applicable Qualifying Period. The Offer is not exchangeable for cash. The donation made by AIA Health to the MDCF is not tax deductible for the Eligible Customer. See full terms and conditions here.